Yes, This Is Already a Global Financial Crisis

Did you know that 11 trillion dollars in global stock market wealth was wiped out during the third quarter of 2015? When I was emailed this figure by a friend, I was stunned for a moment. I knew that things were bad, but were they really this bad? When I first received this information, I had just finished a taping for a television show in which I had boldly declared that 5 trillion dollars of stock market wealth had been wiped out around the world. Unfortunately, the final number has turned out to be much larger than that. Over the past three months, the stock markets of all major global economies have been crashing simultaneously, and 11 trillion dollars of “paper wealth” has now completely vanished. The following comes from Fortune…

Did you know that 11 trillion dollars in global stock market wealth was wiped out during the third quarter of 2015? When I was emailed this figure by a friend, I was stunned for a moment. I knew that things were bad, but were they really this bad? When I first received this information, I had just finished a taping for a television show in which I had boldly declared that 5 trillion dollars of stock market wealth had been wiped out around the world. Unfortunately, the final number has turned out to be much larger than that. Over the past three months, the stock markets of all major global economies have been crashing simultaneously, and 11 trillion dollars of “paper wealth” has now completely vanished. The following comes from Fortune…Global equity markets suffered a bruising third quarter, shedding $11 trillion worth of global shares over three months, according to Bloomberg. It was the market’s worst quarter since 2011. The prolonged slump was due to low prices for commodities such as oil, instability in China’s markets, and the anticipation that the U.S. Federal Reserve will soon raise interest rates.In light of this number, how in the world is it possible that there is still anyone out there that is claiming that “nothing happened” over the past few months? In China, they sure aren’t claiming that “nothing happened”. Chinese stocks are down about 40 percent from the peak of the market. In Germany, they sure aren’t claiming that “nothing happened”. As of a few days ago a quarter of all German stock market wealth had been wiped out since the peak earlier this year. Yes, things have been a bit milder in the United States. So far, stocks are only down about 10 percent or so, but we did see some truly remarkable things happen over the past three months. We witnessed the 8th largest single day stock market crash on a point basis in U.S. history, we witnessed the 10th largest single day stock market crash in U.S. history, and we witnessed the single greatest intradaystock market crash in all of U.S. history. On August 24th the Dow plunged 1,089 points before bouncing back. But every time the markets have an up day there are all these people running around declaring that “the crash is over”. Well, that is not how financial markets work. They “stair-step” on the way up and they do the same thing on the way down. And without a doubt, U.S. stocks still have a long, long way to go down.

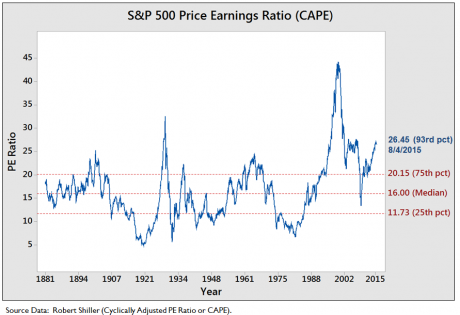

In recent years, stocks have soared to unbelievably unrealistic levels. One of the most popular methods of measuring the true value of stocks is something called the cyclically-adjusted price to earnings ratio. It was developed by economist Robert Shiller of Yale University, and it attempts to accurately show how much we are paying for stocks in relation to how much those corporations are actually earning. When this number is very high, stocks are overvalued, and when this number is very low stocks are undervalued.

Earlier this year, CAPE hit a peak of about 27, and by the beginning of August it was still sitting up around 26. The only times CAPE has been higher has been just before other stock market bubbles have been burst…

It would take a total drop of about 40 percent from the peak of the market just to get back to average. So far the Dow has fallen about 10 percent or so, so it is going to take another 30 percent crash just to get to a point where stock prices are considered “normal” once again. Another very common measurement of stock values shows the exact same thing. The ratio of corporate equities to GDP is also known as “the Buffett Indicator” because Warren Buffett loves it so much. When stock prices get very high in relation to the size of the overall economy that is a sign that stocks are overvalued, and when stock prices get very low in relation to the size of the overall economy that is a sign that stocks are undervalued. The chart below was recently posted by dshort.com and it shows that stock prices would have to fall more than 40 percent just to get back to the historical average (the mean).

Right now, lots of Americans are rushing to get back into the stock market because “September is over” and they figure that stocks are a good value now since they have gone down a good bit. But as you can clearly see from the charts that I have just shared, U.S. stocks are still a terrible value. Even if we don’t experience a “black swan event” like a major natural disaster, a large scale terror attack or the collapse of a globally important financial institution in the months ahead, it is inevitable that stocks will go down a lot more at some point. Stocks simply cannot defy gravity forever. These bubbles have always ended in crashes in the past, and the same thing is going to happen again this time. People that are trying to tell you that “things are different this time” simply refuse to learn from history.

I am writing this piece while waiting for a plane at Denver International Airport. I missed my connection because my first flight was delayed by about an hour. So I am just sitting here watching people walk past. Most of them are just living their lives without any idea of the disaster that is about to hit this country. Over the past few days I have been reflecting on the fact that our nation has willingly chosen this path. We willingly chose to go into so much debt. We willingly chose to send millions of good paying jobs overseas. We willingly chose to pump up these financial bubbles. We willingly chose to reject the values of our forefathers. We willingly chose men like Barack Obama, Harry Reid and John Boehner to represent us in Washington. The things that are coming are the logical consequences for decisions that we have collectively made as a nation. There are still many out there that do not believe that we will have to face any consequences for what we have done. Unfortunately for all of us, they are not going to have to wait very long at all to see how incredibly wrong they were.

I am writing this piece while waiting for a plane at Denver International Airport. I missed my connection because my first flight was delayed by about an hour. So I am just sitting here watching people walk past. Most of them are just living their lives without any idea of the disaster that is about to hit this country. Over the past few days I have been reflecting on the fact that our nation has willingly chosen this path. We willingly chose to go into so much debt. We willingly chose to send millions of good paying jobs overseas. We willingly chose to pump up these financial bubbles. We willingly chose to reject the values of our forefathers. We willingly chose men like Barack Obama, Harry Reid and John Boehner to represent us in Washington. The things that are coming are the logical consequences for decisions that we have collectively made as a nation. There are still many out there that do not believe that we will have to face any consequences for what we have done. Unfortunately for all of us, they are not going to have to wait very long at all to see how incredibly wrong they were.

{kind=link}